Why invest?

Whitbread is the UK’s largest hospitality business, employing c.31,500 people and a long-time constituent of the FTSE100. Premier Inn is the largest hotel brand in the UK and has a growing presence in Germany. Our proposition is synonymous with providing high-quality and great value hotel rooms for our guests, and food and beverage (F&B), especially a hot breakfast, is a key part of the guest experience at Premier Inn.

The following are key elements of our investment case:

1) Long-term growth opportunity in the UK

Whilst we are already the clear market leader, we have significant growth potential to reach up to 125,000 rooms across the UK and Ireland. With a material reduction in independent supply following the pandemic and a subdued pipeline of new build hotels, we do not expect UK supply to recover to 2019 levels until at least 2028. Our flexible approach to property ownership means we are well placed to take advantage of this significant market opportunity by adding rooms at attractive rates of return through both new sites and extensions, as demonstrated by our Accelerating Growth Plan (AGP).

Open rooms

> 86000

2030/31 open rooms target

96000

Long-term potential rooms

125000

2) Unlocking value in Germany

Germany is a large and exciting market with significant volumes of leisure and business travel. The independent sector is larger than in the UK and has also been in decline. However, there is no clear leader in the branded budget segment, creating opportunity for Premier Inn. Having grown rapidly through a combination of acquisitions, conversions and new builds, we have 65 open hotels and with our committed pipeline are set to become one of the largest operators in Germany with a clear focus on accelerating returns by 2030/31.

Open rooms

> 11000

2030/31 open rooms target

18000

Long-term ambition

No. 1

3) Differentiated model underpins a market-leading proposition

Our operating model is a key source of competitive advantage. Being in control of all aspects of our operations ensures the delivery of a consistent, high‑quality product, whilst our scale and financial discipline mean we can continue to offer great value for our guests and attractive returns for our shareholders. A centralised approach to revenue management allows us to maximise revenue whilst managing our cost of sales by integrating our digital marketing and customer relationship management activity into our trading strategy. Our food and beverage offer is a key part of our proposition, especially a hot breakfast, and helps us to drive incremental revenue per available room (RevPAR). Our Force for Good sustainability programme ensures we are contributing positively to the communities where we operate and helps mitigate potential climate-related risks.

UK YouGov Brand Index1

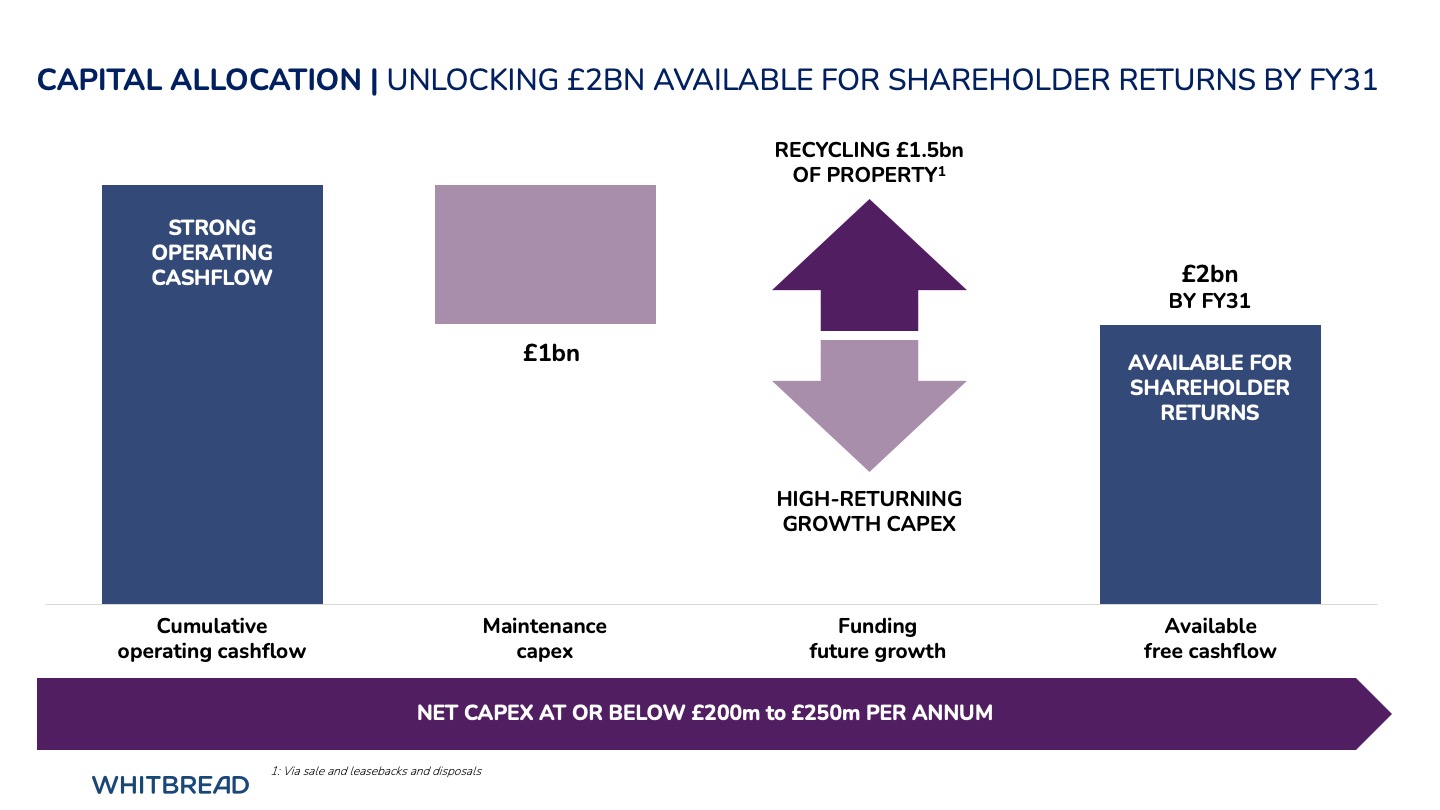

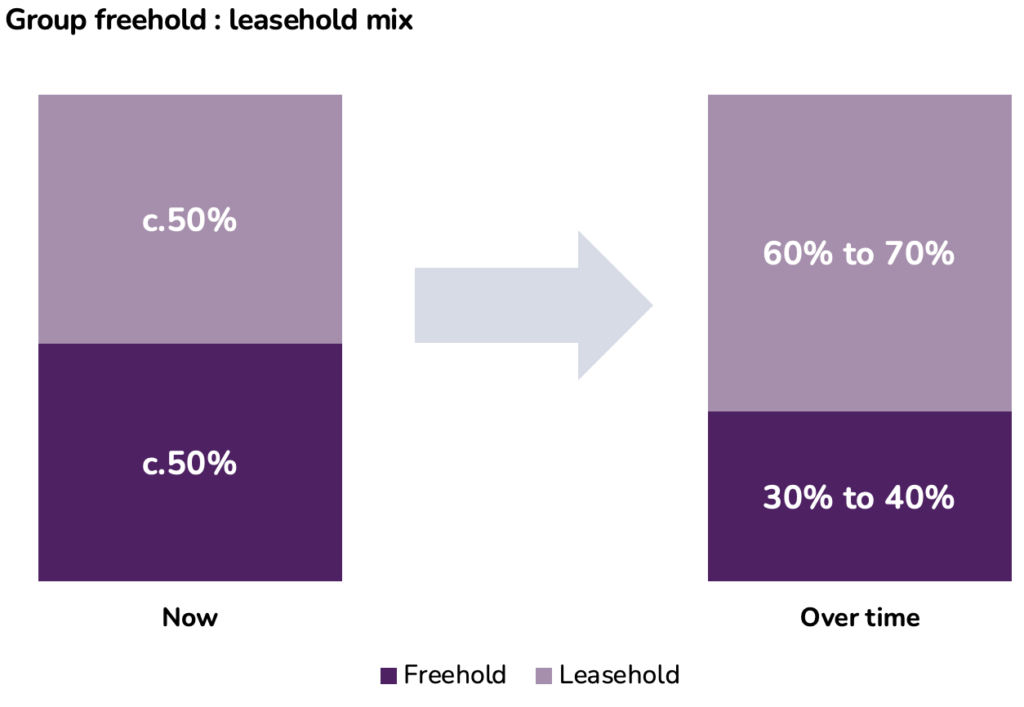

4) Asset-backed balance sheet provides stability and enables growth

Retaining a flexible approach to property ownership and a strong balance sheet have allowed us to keep financing costs low whilst also providing significant commercial benefits, in the form of a strong financial covenant and being able to maximise site returns through our value creation cycle. Whilst the Group will continue to benefit from owning a substantial amount of freehold real estate, we will reduce the proportion held from c.50% in 2025/26 to 30% – 40% over time. We will recycle £1.5bn of our freehold property via sale and leasebacks and other disposals, to fund future growth and increasingly look to grow on a leasehold basis over the life of our New Five-Year Plan.

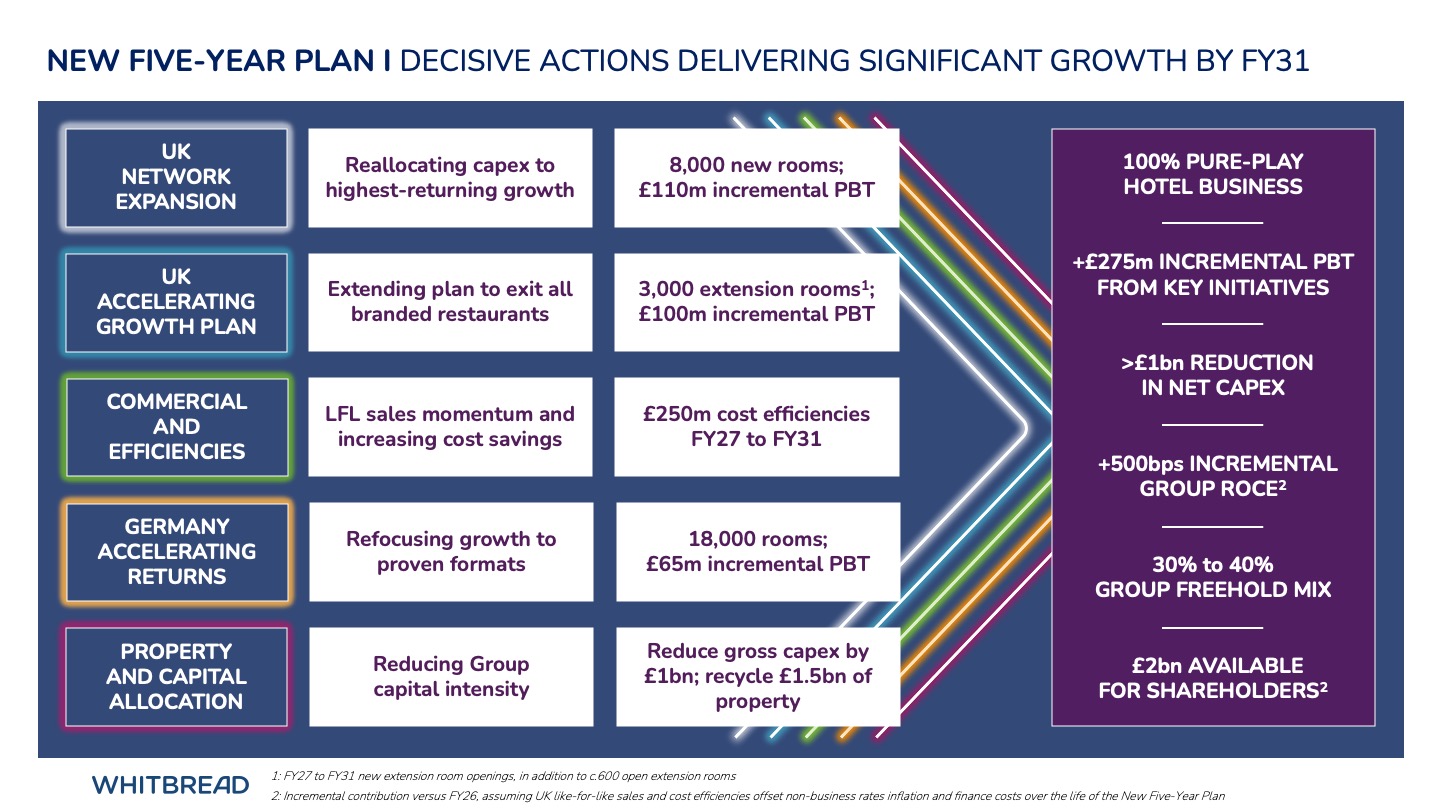

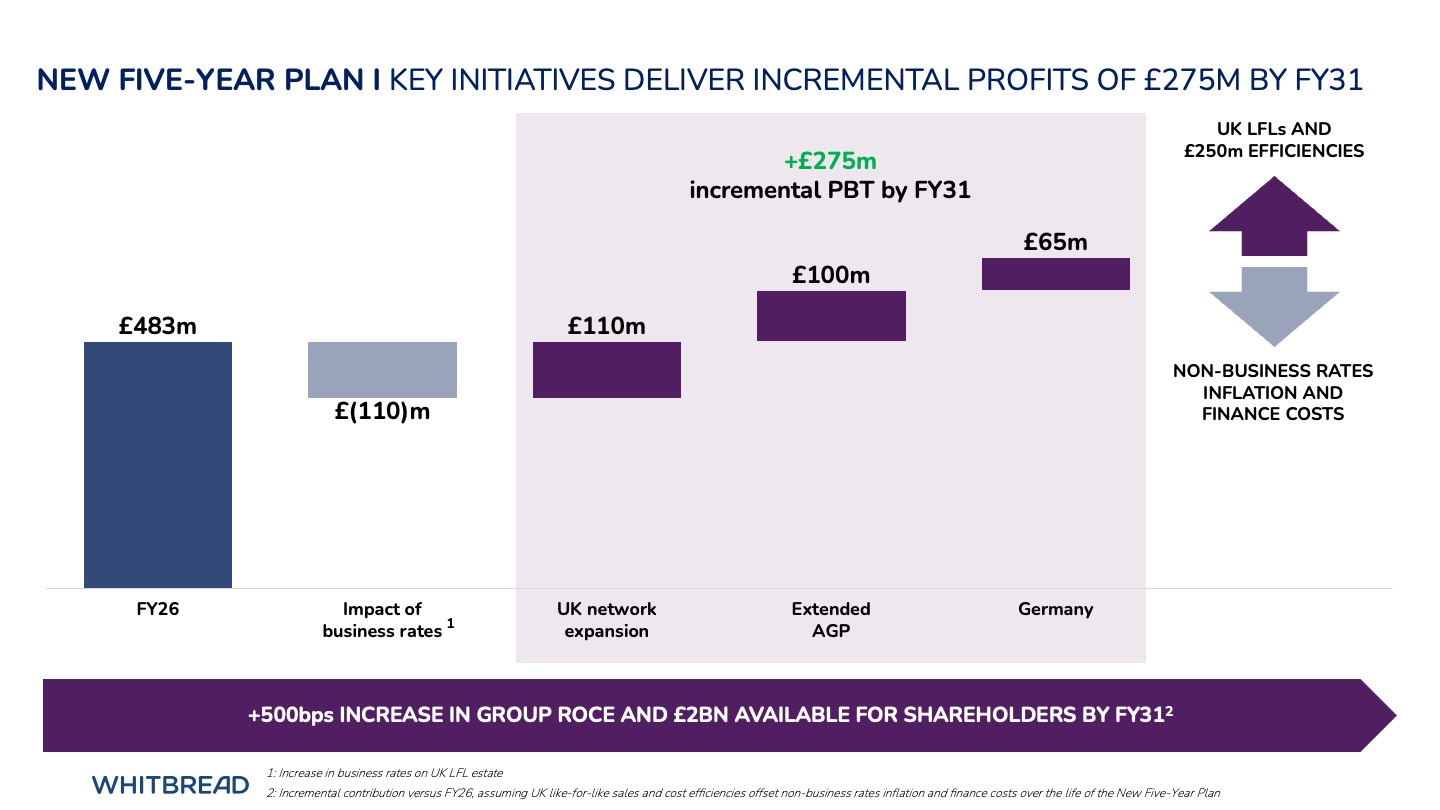

5) New Five-Year Plan to maximise shareholder returns

In response to a series of unexpected fiscal and macroeconomic headwinds, we undertook a detailed business review and have announced a New Five-Year Plan to 2030/31. This will extend our market-leading position in the UK, accelerate cash flow and returns in Germany and deliver long-term value creation for shareholders. With a reduced level of capital intensity, a reduction in the amount of freehold property held by the Group and the expected increase in profitability over the life of the plan, our New Five-Year Plan is designed to maximise shareholder returns over the medium and long term.